Do you ever wonder where you stand financially, really? Like, if you added up everything you own and subtracted everything you owe, what number would you get? Knowing how to calculate your net worth is, you know, a pretty big deal. It's like taking a financial snapshot of your life right now, giving you a clear picture of your economic standing. This number isn't just for rich people; it's a vital tool for anyone wanting to get a handle on their money and plan for the future, so to speak.

Your net worth is, essentially, the value of all your assets minus all your liabilities. It’s a simple equation, yet it tells a powerful story about your financial journey. Some people find the idea a bit intimidating, but honestly, it’s a straightforward process that anyone can do, and it provides such a useful baseline for financial health.

This guide will walk you through each step of finding your net worth. We'll break down what counts as an asset, what falls under liabilities, and how to put it all together. You'll discover why this calculation is so important for setting goals and making smart money choices. It's really about giving you the tools to feel more in control of your financial life, which is, you know, a pretty good feeling.

Table of Contents

- What Exactly is Net Worth?

- Why Knowing Your Net Worth Matters

- Step-by-Step: How to Calculate Your Net Worth

- Tips for a More Accurate Calculation

- What Your Net Worth Number Means

- Frequently Asked Questions About Net Worth

What Exactly is Net Worth?

Net worth is, quite simply, a measure of your financial health at a specific moment. It’s a number that shows you what you truly own once you take away what you owe. Think of it like this: if you sold everything you have and paid off all your debts, what would be left? That remaining amount is your net worth. It’s a very personal number, and it changes over time, too.

Assets: What You Own

Assets are things of value that you possess. These are items or accounts that could, in theory, be turned into cash. They represent what you own and contribute positively to your net worth. It's important to be thorough when listing these, as every bit adds up, you know?

- Cash and Equivalents: This includes money in your checking accounts, savings accounts, money market accounts, and any physical cash you keep. It’s the most straightforward type of asset.

- Investments: Think about your retirement accounts like 401(k)s, IRAs, or Roth IRAs. Also include brokerage accounts, mutual funds, stocks, bonds, and any other investment vehicles you might have. Even small investments count, as a matter of fact.

- Real Estate: The market value of your home, any rental properties, land, or other real estate you own. This can be a significant part of many people's assets, obviously.

- Vehicles: The current market value of your cars, motorcycles, boats, or other vehicles. Remember, these typically depreciate over time, so use a current estimated value.

- Personal Property: This can include valuable jewelry, art, collectibles, or even high-value electronics. For the most part, you only need to list items that have significant resale value, not every single thing you own, typically.

- Other Assets: Any other valuable items or accounts, such as a business you own, intellectual property, or even a pension plan's current value.

Liabilities: What You Owe

Liabilities are your debts or financial obligations. These are amounts of money you owe to others, and they reduce your net worth. It’s important to list all of them, even the small ones, to get an accurate picture, you know.

- Mortgages: The outstanding balance on your home loan or any other property loans. This is often the largest liability for many people, naturally.

- Credit Card Debts: The total balance you owe across all your credit cards. These can add up quickly, so it's good to keep track, really.

- Student Loans: The remaining balance on any student loans you have.

- Car Loans: The outstanding balance on any loans used to purchase vehicles.

- Personal Loans: Any money borrowed from banks, credit unions, or individuals.

- Medical Debts: Any outstanding bills from medical procedures or services.

- Other Debts: This could include lines of credit, tax debts, or any other money you are obligated to pay back.

Why Knowing Your Net Worth Matters

Calculating your net worth is far more than just a math exercise; it’s a powerful financial management tool. It gives you a clear, objective view of your financial standing, which is pretty essential for making informed decisions. It’s like a financial report card that you create for yourself, and it can be incredibly motivating, you know.

Tracking Progress

One of the biggest benefits of knowing your net worth is the ability to track your financial progress over time. When you calculate it regularly, say once a year, you can see if your efforts to save more, invest wisely, or pay down debt are actually working. A rising net worth shows you’re moving in the right direction, which is, you know, a very encouraging sign. It's a tangible way to see your financial health improve, or perhaps identify areas that need a little more attention, at the end of the day.

Setting Goals

Your net worth figure provides a fantastic baseline for setting financial goals. Whether you want to save for a down payment on a house, plan for retirement, or just achieve a certain level of financial freedom, knowing your current net worth helps you understand how far you have to go. It allows you to create realistic and achievable targets, giving you a clear path to follow. For example, if you want to reach a certain net worth by a specific age, this calculation helps you map out the steps needed to get there, like your own financial roadmap, essentially.

Making Informed Choices

When you understand your net worth, you’re better equipped to make smart financial choices. Should you take on more debt? Can you afford that new purchase? Is now the right time to invest more? Your net worth gives you context for these decisions. It helps you avoid overextending yourself and encourages responsible spending and saving habits. It’s really about having a solid foundation of information, which, you know, makes all the difference when money is involved.

Step-by-Step: How to Calculate Your Net Worth

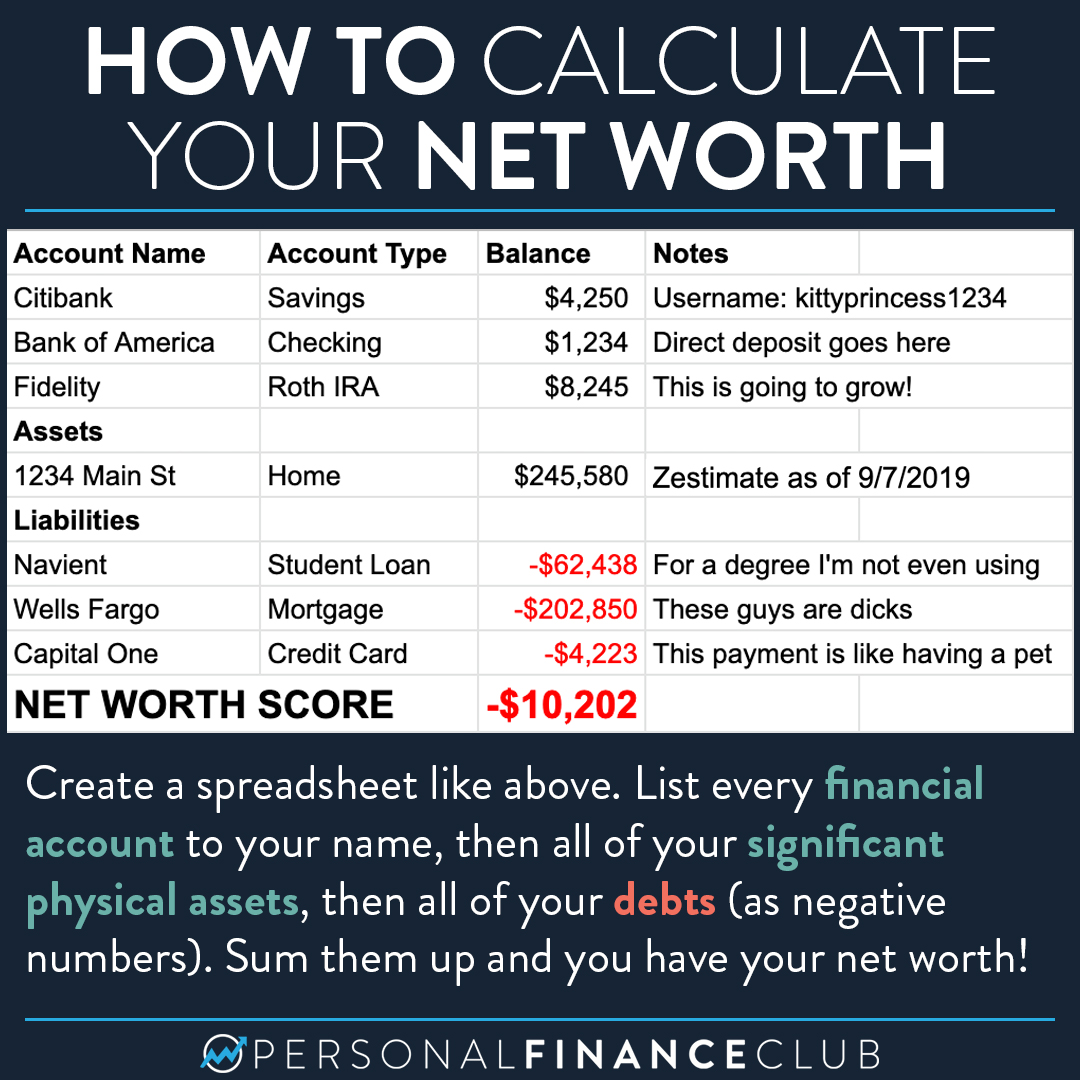

Now, let's get down to the actual calculation. It’s a straightforward process, honestly, and you don’t need any fancy math skills. Just a bit of organization and some simple arithmetic. Our free simple calculator, like your basic handheld calculator, can certainly help with the addition and subtraction needed here, or you could use a spreadsheet, too.

Step 1: List All Your Assets

The first step is to gather all the information about what you own. Be as comprehensive as possible, but don't overthink the exact value of every small item. Focus on the big ones. You'll want to list the current market value for each item, not what you paid for it. This might involve checking online resources or recent statements, you know.

Liquid Assets

Start with the easiest things to value: your cash. This includes money that you can access quickly without much trouble. For example, check your bank statements for your checking account balance, your savings account balance, and any money market accounts. If you have any physical cash, like a little stash at home, include that too. It's usually a pretty simple sum to get, you know, the total here.

Investment Assets

Next, look at your investments. This can take a bit more digging. Pull up statements for your 401(k), IRA, Roth IRA, and any other retirement accounts. Get the current value of your brokerage accounts, including stocks, bonds, and mutual funds. If you have any other investments, like a certificate of deposit (CD) that hasn't matured, add its current value. Our scientific calculator, for instance, can help evaluate percentages if you need to figure out growth on some of these, but usually, the statement gives you the current number, which is pretty handy.

Personal Property

This category is where you list things like your home, vehicles, and other valuable possessions. For your home, you'll need its estimated market value. You can often get a good idea from online real estate sites or by looking at comparable homes that have sold recently in your area. For vehicles, check online valuation guides like Kelley Blue Book or Edmunds to get a current resale value. For other valuable items like jewelry, art, or collectibles, use their estimated resale value. Don't worry about valuing every piece of furniture or clothing; focus on items with significant worth, which is, you know, usually the best approach.

Step 2: List All Your Liabilities

Once you have a good handle on your assets, it’s time to list everything you owe. This means gathering statements for all your debts. Just like with assets, be thorough here. Every debt, big or small, needs to be accounted for to get an accurate picture, which is, you know, really important.

Short-Term Debts

These are debts you expect to pay off relatively quickly, usually within a year. The most common example is credit card debt. Get the total outstanding balance from all your credit card statements. Also, include any personal loans that have a short repayment period or any medical bills that are due soon. Sometimes, people have a line of credit they've drawn on; that would go here too. It’s important to be honest with yourself about these amounts, you know, for the most accurate calculation.

Long-Term Debts

These are debts that typically take many years to pay off. The biggest one for many people is their mortgage. Find your latest mortgage statement and note the outstanding principal balance. Also, include any student loans you have, noting their current balance. If you have a car loan, get the current payoff amount for that too. Other long-term debts could include business loans or home equity lines of credit. It's really about getting a complete picture of everything you still owe, you know, over the long haul.

Step 3: Do the Math

This is where it all comes together. Once you have your total assets and total liabilities, the calculation is incredibly simple. It’s just one basic arithmetic step. You take your total assets and subtract your total liabilities. Our free simple calculator, or even our online scientific calculator, can help you quickly and accurately perform this arithmetic. It’s just addition and subtraction, really, so anyone can do it.

The formula is:

Total Assets - Total Liabilities = Net Worth

For example, let’s say your total assets add up to $300,000. This might include your home equity, savings, and investments. And let’s say your total liabilities, like your mortgage balance, student loans, and credit card debt, add up to $150,000. Your net worth would be $300,000 - $150,000 = $150,000. It’s a very clear way to see where you stand, which is, you know, the whole point.

Tips for a More Accurate Calculation

While the process of calculating your net worth is simple, getting the most accurate number requires a bit of attention to detail. These tips can help ensure your snapshot is as true to life as possible, which is, you know, what you really want.

Gather Your Documents

Before you start, collect all necessary financial statements. This includes bank statements, investment account statements, mortgage statements, credit card bills, and loan statements. Having everything in front of you makes the process much smoother and reduces the chance of missing anything. It’s like preparing all your ingredients before you start cooking; it just makes everything easier, honestly.

Be Realistic

When valuing assets, especially things like your home or car, try to be realistic about their current market value. Don't overestimate what something might sell for, and don't underestimate what you owe. Using current, objective data sources for valuations, rather than just guessing, is key. It’s important to avoid wishful thinking here, which is, you know, pretty common but not helpful for accuracy.

Update Regularly

Your net worth is not a static number; it changes constantly as you earn, spend, save, invest, and pay down debt. It’s a good idea to recalculate your net worth at least once a year, maybe around the same time each year, like your birthday or the start of a new year. This allows you to see trends and understand the impact of your financial decisions over time. Some people even do it quarterly, which is, you know, a very dedicated approach. Regular updates help you stay on track and adjust your plans as needed.

What Your Net Worth Number Means

Once you have your net worth number, you might wonder what it actually tells you. It’s not just about the number itself, but what it represents about your financial journey. It’s a very personal metric, and its meaning can vary for everyone, you know.

Positive Net Worth

If your total assets are greater than your total liabilities, you have a positive net worth. This means you own more than you owe, which is, you know, generally a good sign of financial health. A positive net worth indicates that you are building wealth and are on a path towards financial security. It shows that your financial habits are likely leading you in a good direction, which is, you know, something to feel good about.

Negative Net Worth

If your total liabilities are greater than your total assets, you have a negative net worth. This is common for younger individuals, especially those with significant student loan debt or a new mortgage. It means you owe more than you own. While it’s not ideal, a negative net worth is not necessarily a sign of failure. It simply means you have work to do to build up your assets and reduce your debts. It’s a starting point, essentially, and it gives you a clear target to aim for, which is, you know, really helpful.

It's a Snapshot

Remember, your net worth is just a snapshot in time. It doesn't tell your whole financial story, like your income or your spending habits. It's a single data point. The real value comes from tracking it over time to see progress and make adjustments. A single number doesn't define your financial future, but it's a very useful tool for guiding it. It's about the trend, really, rather than just one specific number on one specific day.

Frequently Asked Questions About Net Worth

Here are some common questions people ask when they're figuring out their financial standing.

Is net worth calculated monthly or yearly?

Most people calculate their net worth yearly. This provides a good balance between seeing progress and not getting bogged down in too much detail. Doing it monthly might be a bit much for most, as values don't change that drastically day to day, you know. However, if you're making big financial moves, like paying off a large debt or making a major investment, a more frequent check-in could be useful, perhaps quarterly.

What counts as an asset for net worth?

Assets include anything you own that has financial value and could be converted into cash. This means your cash in bank accounts, investments like stocks and retirement funds, real estate (your home, rental properties), vehicles, and valuable personal possessions like jewelry or art. It’s basically anything that adds to your wealth, which is, you know, pretty straightforward.

What is a good net worth for my age?

There isn't a single "good" net worth for any age, as it really depends on many personal factors like income, location, and life goals. Financial experts often suggest aiming for a positive and growing net worth. For example, some guidelines might suggest having a net worth equal to your annual salary by age 30, or two times your salary by age 35, and so on. But these are just general guidelines, you know, and your personal situation is what truly matters. The most important thing is that your net worth is moving in a direction that supports your own financial aspirations.

Understanding what net worth means is a great first step. Learn more about calculators on our site, and link to this page for more financial tools.

:max_bytes(150000):strip_icc()/net-worth-4192297-1-6e76a5b895f04fa5b6c10b75ed3d576f.jpg)

Detail Author:

- Name : Minerva Dibbert

- Username : mccullough.lavonne

- Email : jeramy20@hayes.com

- Birthdate : 1993-06-08

- Address : 9198 Justus Parkway Brekkeport, VA 84617

- Phone : +1.513.322.8515

- Company : Okuneva-Goldner

- Job : Operating Engineer

- Bio : Qui voluptates eos adipisci rerum quis porro. Aliquid ducimus doloribus ut ut velit. Doloremque ipsum itaque sit est libero.

Socials

twitter:

- url : https://twitter.com/lraynor

- username : lraynor

- bio : Quas voluptas ea temporibus tempore. Qui sunt facere ut qui. Minima et dolore est ratione fugit est.

- followers : 3261

- following : 885

linkedin:

- url : https://linkedin.com/in/lawson_real

- username : lawson_real

- bio : Est qui similique quasi possimus nihil.

- followers : 4680

- following : 514